Generating revenue with embedded finance

More and more brands are choosing to use embedded financial technology for their financial services programs. Major brands like Starbucks, Walgreens, Dollar General, Uber, and Boost Mobile are all using different types of embedded financial services in different parts of their customer journeys to drive innovation and customer retention.

While end consumers appreciate the improvements to financial experiences and rewards programs, brands who take this innovative leap have an additional motivation — creating new streams of revenue.

We should note that brands have been partnering with financial institutions to offer “branded financial services” for a long time and making good money doing so. But those models are changing.

Innovation has a great way of making things quickly look obsolete, and embedded finance technology has made the traditional brand/financial institution partnership outdated.

Brands offering financial products and services isn't new

Historically, if a brand wanted to offer their customers financial services (cards, loans, money remittance), it would have to formally partner with a bank and a network sponsor.

In this traditional arrangement, brands bring their logo, recognition, and customers to the table, while banks and network providers bring the financial components. A match made in heaven, right? Not so fast.

While these partnerships work (and have been working for a long time), brands consistently run into issues with program personalization because they have to abide by the financial institution's rules and guidelines. The rewards, customer experiences, and, most importantly, the revenue opportunity are controlled by the bank sponsoring the program.

Example: Co-branded cards

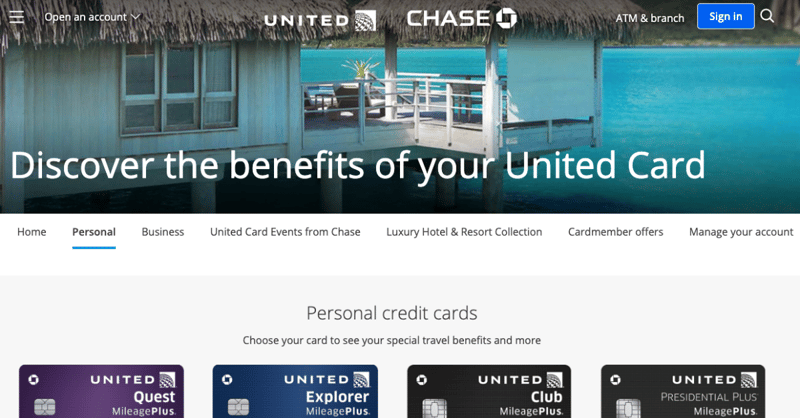

We’re all familiar with co-branded cards. Whether it be the Target Red Card or the United Explorer Card, these cards are the go-to financial service for brands with large customer bases.

Brands make money from co-branded cards through sign-up bounties and revenue share. In most cases, co-branded cards are strong revenue generators for brands. However, when you pull back the curtain on these cards, it becomes evident that brands are giving their customers to the traditional financial institution backing the co-branded card program.

Case in point: The United Explorer Card. The card’s benefits are tied back to spending with United Airlines (and program partners), but the entire financial experience is housed within their bank sponsor, Chase.

Consumers apply for the card through Chase, pay bills, book travel, and access rewards through the Chase app.

The long-term value of co-branded card programs is captured by the bank as they are acquiring new customers at a lower cost, making money off the card program, and can offer these card program customers new financial products in the future.

Taking the innovative route and launching a card program with embedded finance technology instead of a traditional financial institution partnership creates opportunities to generate more revenue on the card program — and build long term customer loyalty.

Beyond co-branded card programs, the advantages of using embedded finance technology to deliver financial services span all types of products. Below, we’ll dive into the different elements of a program that generate new streams of revenue.

Four new streams of revenue unlocked

As you start to model the revenue projections around your program, you’ll come across all types of line items like transactions, one-time fees, and administrative fees.

When you use embedded finance technology to create your financial service program, it’s important to remember that you own the program from end-to-end. This means you can choose to charge (or not to charge) for different line items within a program. These choices impact the end-customer experience, and also the end-revenue number:

Here’s a breakdown of the different sources of revenue by offering financial services using embedded finance technology.

1. Transactions

Swipe fees, commonly referred to as interchange, are percentages of total card transactions that get pushed to the parties that make the transaction possible.

Interchange is variable but can be estimated at 1-3 percent of the transaction. Traditionally, interchange is split between the card issuer, the consumer’s bank, the merchant’s bank, and the networks that process the transaction.

Issuing cards using embedded finance technology makes you the card issuer. This means you’re a beneficiary of part of the interchange split.

Transactions don’t have to only be for card usage. Adding advanced features like in-app savings creates opportunities to capture revenue on funds that are held on the card.

2. Money movement

Some programs charge fees associated with money movement. Here are the most common line items that generate revenue for money movement:

- Cash loading from an ATM

- ATM withdrawals

- Out-of-network transfers

- Mobile check deposits

- Deposits into their brand account via a debit or credit card

3. International payments

Offering customers a low-cost way to send money to friends and family across borders is a crucial financial service for many people living in the United States. Opportunities to generate revenue through a global payments program include:

- Fixed and variable fees for sending money (~4% based on amount and destination)

- Exchange rates on currency conversions

4. Interest

As consumers add funds to an account or wallet, businesses offering these financial products benefit from the interest on those funds. Pre-funding debit cards for future purchases, Save Now, Buy Later, and other opportunities to hold funds, brings yield.

The opportunity to generate revenue from these types of financial services is vast. Programs can take many forms, but at the end of the day, it’s all about delivering your customers more value.

Beyond revenue: The value of embedded finance

New streams of revenue are just one part of the value chain.

Beyond revenue, embedded finance technology offers visibility into customer spending patterns that can bring innovation to the way you design your customer experiences, capture customer insights, and more.

Read the Buyer's Guide: Key considerations in selecting an embedded finance provider

Whether you're looking for new ways to innovate and drive new revenue, grow your loyalty program, improve customer experiences, or just want to learn more, the Buyer's Guide has the answers.

You’ll learn:

- Banks, BaaS,Embedded Finance and how they they differ

- Must have attributes of embedded finance providers

- What to know before your DIY

- Compliance and regulatory requirements